When purchasing insurance in Hong Kong, there are generally two types of insurance salespeople that you may encounter: insurance agents and insurance brokers.

What are the differences in their roles or responsibilities? Do they need to register with recognized organizations before working? And what are their professional qualifications?

This article will answer these questions one by one.

In Hong Kong, both companies and individuals must hold an insurance license to conduct insurance business.

Licensed insurance intermediaries in Hong Kong are divided into licensed insurance agents and licensed insurance brokers.

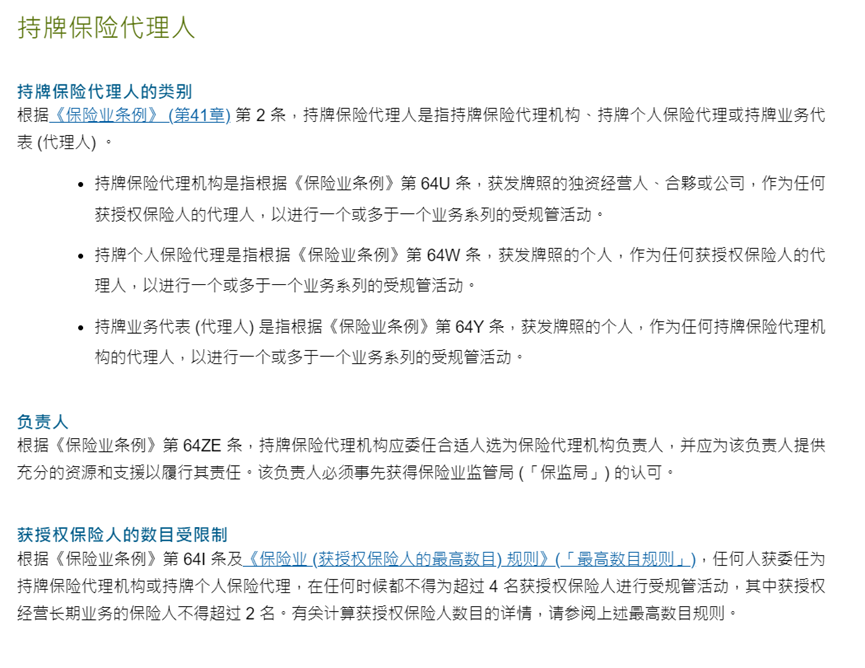

1.Licensed Insurance Agents

Licensed insurance agents include licensed individual insurance agents, licensed insurance agency and licensed responsible officers (agents).

Licensed individual insurance agents and licensed insurance agencies are authorized agents appointed by authorized insurers (i.e. insurance companies), with the insurance companies being their principals. They promote, offer advice, and make arrangements for policies provided by the appointed insurance companies.

Licensed responsible officers (agents) are agents appointed by licensed insurance agencies (i.e. licensed insurance agencies are their principals). They promote, offer advice, and make arrangements for policies provided by the appointed insurers of licensed insurance agencies.

In addition, insurance agents are divided into independent agents and employed agents according to the contract signed with insurance companies.

Employed agents have an employment relationship with a single insurance company and may receive a base salary, as well as commissions and bonuses.

Independent agents do not have an employment relationship with the insurance company they represent. They are appointed to sell insurance products and provide after-sales service by the insurance company and earn commissions from each policy arranged.

Independent licensed individual insurance agents cannot represent more than four insurance companies at the same time, with a maximum of two being life insurance companies.

Both independent and employed agents can represent insurance companies, explain the application process to customers, prepare and submit relevant insurance documents, manage policies, and assist policyholders in making claims.

The commission of insurance agents is calculated as a percentage of the premium, with the amount usually decreasing as the policy term gets longer. For example, for a 10-year policy, the agent may receive a commission of about 25% to 40% of the premium in the first year, which will decrease to about 7% to 5% in the second year, and will be 0% in the fifth or sixth year.

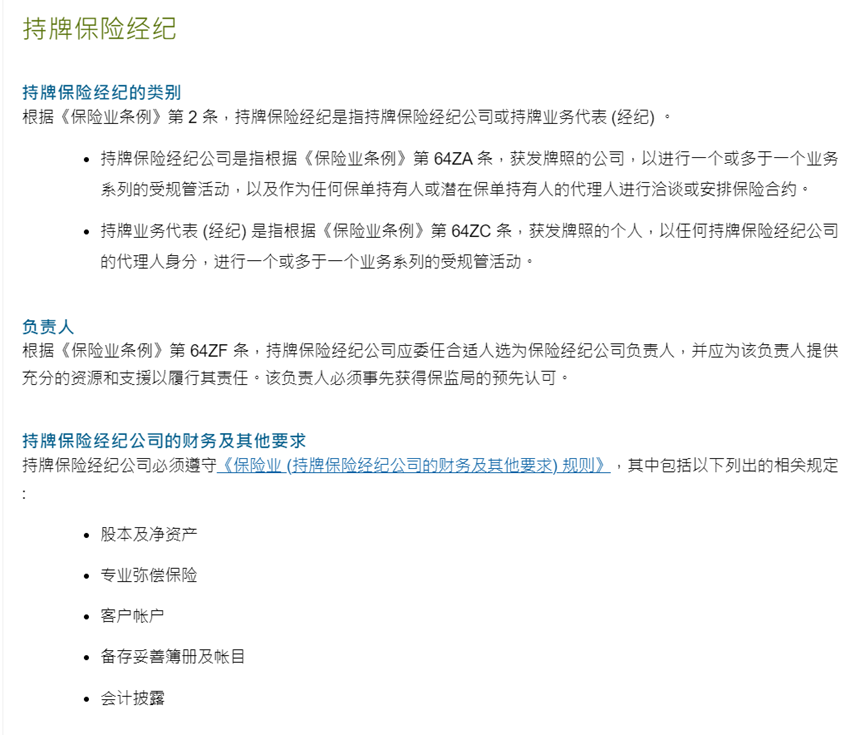

2.Insurance Brokers

Licensed insurance brokers include licensed insurance brokerage firms and licensed business representatives (brokers).

Licensed insurance brokerage firms provide advice on policies to clients and act as their agents in handling policy-related matters, including the purchase, negotiation, and arrangement of policies with insurance companies. They can collaborate with multiple insurance companies simultaneously, acting as a liaison between the policyholder and the insurance company, and recommend and sell insurance products based on the policyholder’s needs.

Licensed business representatives (brokers) are appointed representatives of licensed insurance brokerage firms (i.e., representing licensed insurance brokerage firms). In this capacity, they provide advice on policies to clients and represent the licensed insurance brokerage firm that appointed them in handling policy-related matters on behalf of their clients.

In common parlance, an insurance broker usually refers to a licensed business representative of a licensed insurance brokerage firm, also known as a broker.

The income of insurance brokers in Hong Kong typically comes from commissions paid by insurance companies, not clients. Insurance brokerage firms usually receive a one-time commission from insurance companies after the policy takes effect. For example, signing a new 10-year policy might yield a commission of about 40%-70% of the premium. If the policyholder cancels or reduces coverage within a specified period, the insurance company may also claw back the commission.

In summary, in everyday life, the three main types of licensed insurance intermediaries that we interact with are: licensed individual insurance agents appointed by insurance companies, licensed business representatives (agents) appointed by licensed insurance agency firms, and licensed business representatives (brokers) appointed by licensed insurance brokerage firms.

The primary responsibilities of both licensed insurance agents and licensed insurance brokers are to assist policyholders in understanding, learning about, and buying and selling insurance products.

Among them, licensed insurance brokers represent policyholders, while licensed insurance agents represent insurance companies; licensed insurance brokers can sell products from different insurance companies; licensed insurance agents can only sell products provided by insurance companies; licensed insurance brokers provide fewer after-sales services for insurance companies; licensed insurance agents can usually provide after-sales services directly.

Insurance brokers have an advantage in product diversity, enabling policyholders to access more market information. In contrast, insurance agents represent one or several insurance companies, and they may have a deeper understanding of the company’s insurance products. They may also be more direct and efficient when handling policy or claims-related matters. Both rely on their professionalism and experience to judge and select suitable insurance products for their clients.

Both insurance brokers and insurance agents rely on commissions as their primary source of income.

Finally, it should be noted that individuals or companies cannot act as both insurance agents and insurance brokers simultaneously.

You can verify their identities in the Licensed Insurance Intermediaries Register (Individual).

How can we help?

2CExam provides HKSI LE, IIQE, EAQE and SQE related exam preparation materials. We sell mock question banks for HKSI LE Papers 1, 2, 3, 5, 6, 7, 8, 9, 12 in Chinese and English; and bibles for HKSI LE Papers 1, 2, 6, 7, 8 in Chinese. We also offer 1 on 1 tutorial services. Besides, we have also made free tutorial videos for HKSI LE Papers 1, 2, 6, 7, 8, 12 and posted on public channels such as Youtube/ Bilibili/ Tencent/ Iqiyi. 2CExam has been an exam training expert for years. Should you need any help please visit www.2cexam.com or contact us through:

Phone +852 2110 9644 Email: [email protected] Wechat: hk2cexam WhatsApp: +852 9347 2064

Please support us by leaving comments and likes if you think this article helps you!

You can scan or click on the QR codes to visit our social media.

Latest Article

Categories

過往文章

Contact US

-

Phone:

+852 2110 9644

-

Email:

-

WhatsApp

+852 9347 2064

-

WeChat

hk2cexam

Interesting Articles

How to check the results of HKSI Paper?

How to check the results of HKSI LE Paper? How to check the results of HKSI LE paper? There are two situations for this. The first one is that if you take the exam in Hong Kong, most of them are computer-based exams, and you will know your results immediately after you finish the exam.…

What exam should I take if I want to be a sponsor?

In Hong Kong, unless an individual or company is exempted, If they wish to conduct the ten “regulated activities” defined by the Securities and Futures Ordinance, they need to apply for a license/registration with the Securities and Futures Commission. Type 1: Dealing in securities Type 2: Dealing in future contracts Type 3: Leveraged…

What exam should I take if I want to help customers buy and sell futures and options?

In Hong Kong, unless an individual or company is exempted, if they wish to conduct the ten “regulated activities” defined by the Securities and Futures Ordinance, they need to apply for a license/registration with the Securities and Futures Commission. Type 1 Dealing in securities Type 2 Dealing in futures contracts Type 3 Leveraged foreign…

What exam should I take if I want to help clients buy and sell Hong Kong stocks, US stocks, and bonds?

In Hong Kong, unless an individual or company is exempted, if they wish to conduct ten “regulated activities” defined by the Securities and Futures Ordinance, they need to apply for a license/registration with the SFC. Type 1 Dealing in securities Type 2 Dealing in futures contracts Type 3 Leveraged foreign exchange trading Type…

What exam should I take if I want to sell group insurance, accident insurance and disability insurance with death compensation?

Are group insurance, accident insurance and disability insurance with death compensation general insurance policies or long-term policies? In fact, there is no absolute answer, because an insurance policy with both accident/disability compensation and life insurance components can be general policies or long-term policies, depending on the plan. As in death compensation accident insurance: It…

What exam should I take if I want to sell life insurance, savings life insurance, annuities, and critical illness insurance?

Life insurance, endowment insurance, annuities, and critical illness insurance are all insurances that are particularly related to human life. Life insurance and endowment life insurance are types of insurance that pay consolation money to the beneficiary after the death of the insured. Annuities are closely related to the life of the insured. Basically for…

What exam should I take if I want to sell accident insurance, domestic helper insurance, and medical insurance?

Accident insurance, domestic helper insurance, and medical insurance are all medical-related insurances that are purchased in order to avoid burdening huge (medical) expenses. According to Hong Kong’s “Insurance Ordinance”, general business protection covers 17 categories, including accidents, sickness, and general legal liability. Therefore, if you want to sell accident insurance, domestic helper insurance, and medical…

What exam should I take if I want to sell engineering insurance and liability insurance?

Engineering insurance and liability insurance are insurances designed to avoid huge financial burdens caused by huge losses. Part of the engineering insurance will protect the legal liabilities of causing the third party to be injured or have property losses; while the liability insurance is to compensate for the liabilities derived from causing injuries or losses…

What exam should I take if I want to sell car insurance, water damage insurance, home insurance, property insurance, and marine cargo insurance?

Car insurance, water damage insurance, home insurance, property insurance, and marine cargo insurance are all property insurances that are purchased to cover losses caused by accidents. According to Hong Kong’s “Insurance Ordinance”, general business insurance covers 17 major categories, including land vehicles, ships, fires and natural forces, damage to property, etc. Therefore, if you want…

What is the Use for IIQE Certificates?

Is there any difference between notification of results and a certificate? Do I need to submit both at the same time when I apply for a license? The IIQE notification of results and certificate are two different kinds of proof. The Vocational Training Council (VTC) Institute of Professional Education and Knowledge (PEAK) is responsible…